By

By  July 27, 2023 at 10:04 AM

July 27, 2023 at 10:04 AM

What You Need to Know

- The growing amount of 2023 inflation data now available makes a reasonably reliable prediction of next year's COLA possible.

- Alicia Munnell, director of the Center for Retirement Research at Boston College, puts the increase between 3.0% and 3.8%.

- This would be much lower than previous years but reflects the fact that inflation is finally moderating.

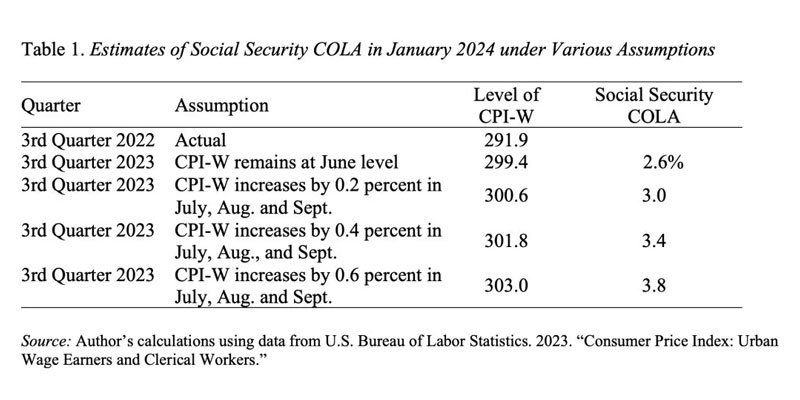

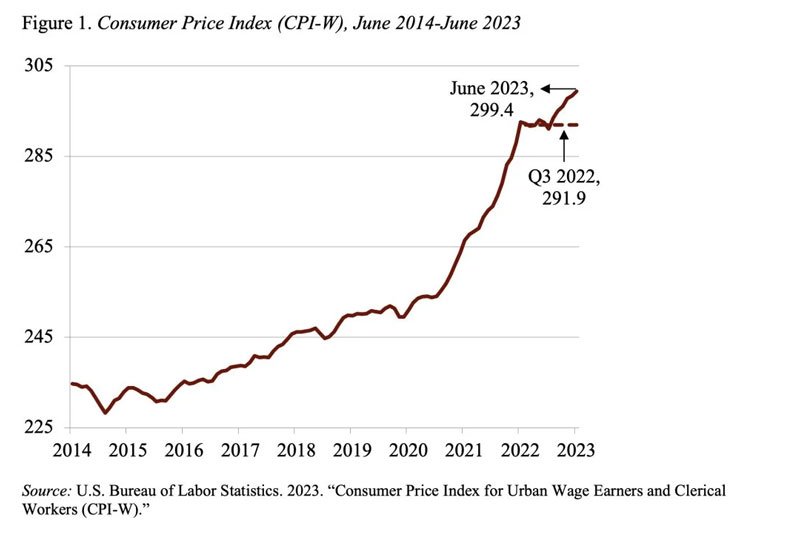

Though it is still too early to calculate the 2024 Social Security benefit cost-of-living adjustment — given that it is based in part on the average increase of the consumer price index for the months of July, August and September — the growing amount of 2023 inflation data now available to prognosticators makes a reasonably reliable projection possible.

According to a new analysis published by Alicia Munnell, director of the Center for Retirement Research at Boston College, retirees should expect a 2024 COLA between 3.0% and 3.8%. For now, Munnell says, she is going with a middle-case 3.4% projection.

This figure puts her roughly in line with the projections made by various other researchers, including Mary Johnson, the Senior Citizens League’s Social Security and Medicare policy analyst, who currently projects the 2024 COLA at 3%. This figure is up from Johnson’s earlier projection of 2.7% from June but still well below the near-record 8.7% COLA for 2023.

“My best guess is the 2024 COLA will be roughly in line with 2024 inflation,” Munnell writes. “In contrast, the COLA over the last two years has been out of sync with actual inflation — too low a COLA in 2021 and too high a COLA in 2022.”

According to Munnell, this pattern is the inevitable result of a backward-looking calculation, but it makes “perfect sense” to base the COLA on actual data rather than a forecast, which could involve constant corrections for over- or under-predicting.

“Most importantly, over the whole inflation cycle, retirees have received the appropriate increase,” Munnell says.

COLA Calculation Basics

As Munnell observes, because the COLA first affects benefits paid after Jan. 1, Social Security needs to have figures available before the end of 2023.