December 29, 2023 at 10:29 AM

December 29, 2023 at 10:29 AM

What You Need to Know

- Three calls — sell U.S. stocks, buy U.S. Treasury bills and purchase Chinese stocks — formed the consensus view.

All across Wall Street, on equities desks and bond desks, at giant firms and niche outfits, the mood was glum. It was the end of 2022 and everyone, it seemed, was game-planning for the recession they were convinced was coming.

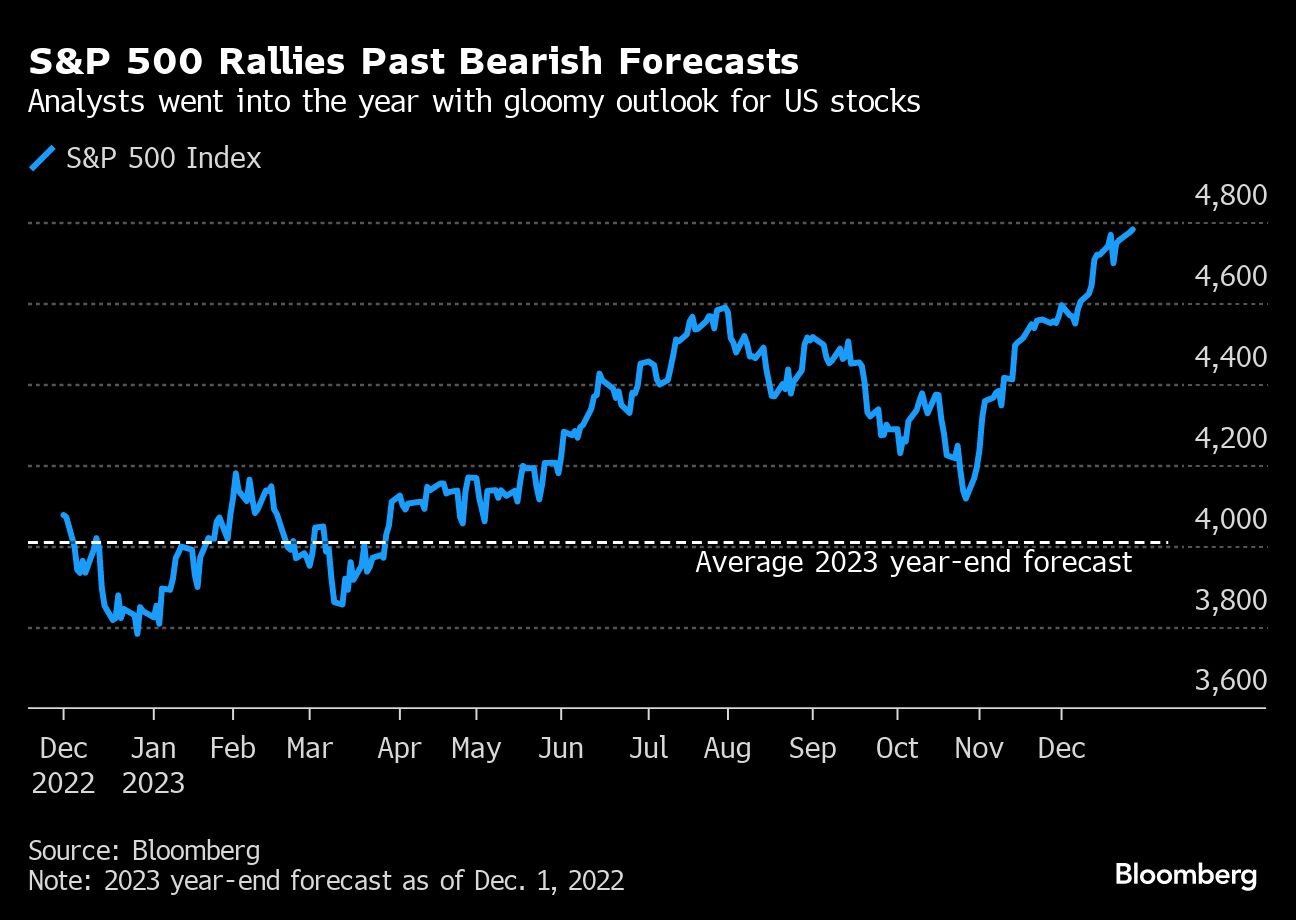

Over at Morgan Stanley, Mike Wilson, the bearish stock strategist who was rapidly becoming a market darling, was predicting the S&P 50O Index was about to tumble.

A few blocks away at Bank of America, Meghan Swiber and her colleagues were telling clients to prepare for a plunge in Treasury bond yields. And at Goldman Sachs, strategists including Kamakshya Trivedi were talking up Chinese assets as the economy there finally roared back from Covid lockdowns.

Blended together, these three calls — sell U.S. stocks, buy Treasuries, buy Chinese stocks — formed the consensus view on Wall Street.

And, once again, the consensus was dead wrong.

What was supposed to go up went down, or listed sideways, and what was supposed to go down went up — and up and up. The S&P 500 climbed more than 20% and the Nasdaq 100 soared over 50%, the biggest annual gain since the go-go days of the dot-com boom.

It’s a testament in large part to the way the economic forces unleashed in the pandemic — primarily, booming consumer demand that fueled both growth and inflation — continue to bewilder the best and brightest in finance and, for that matter, in policy making circles in Washington and abroad.

And it puts the sell side — as the high-profile analysts are known to all on Wall Street — in a very uncomfortable position with investors across the world who pay for their opinions and advice.

“I’ve never seen the consensus as wrong as it was in 2023,” said Andrew Pease, the chief investment strategist at Russell Investments, which oversees around $290 billion in assets. “When I look at the sell side, everyone got burned.”

Money managers at shops like Russell came out looking alright this year, generating returns in stocks and bonds that are slightly higher on average than the gains in benchmark indexes.

But Pease, to be clear, didn’t fare much better with his forecasts than the stars on the sell side. The root of his mistake was the same as theirs: a nagging sense that the U.S. — and much of the rest of the world — were about to sink into a recession.

This was logical enough. The Federal Reserve was in the midst of its most aggressive interest-rate-hiking campaign in decades and spending by consumers and companies seemed sure to buckle.

There have been few signs of that so far, though. In fact, growth actually quickened this year as inflation receded. Throw into the mix a couple of breakthroughs in artificial intelligence — the hot new thing in the world of tech — and you had the perfect cocktail for a bull market for stocks.

S&P 500 & Wilson’s Predictions

The year started with a bang. The S&P 500 jumped 6% in January alone. By mid-year, it was up 16%, and then, when the inflation slowdown fueled rampant speculation the Fed would soon start reversing its rate hikes, the rally quickened anew in November, propelling the S&P 500 to within spitting distance of a record high.

Through it all, Wilson, Morgan Stanley’s chief U.S. equity strategist, was unmoved. He had correctly predicted the 2022 stock-market rout that few others saw coming — a call that helped make him the top-ranked portfolio strategist for two straight years in Institutional Investor surveys — and he was sticking to that pessimistic view.

In early 2023, he said, stocks would fall so sharply that, even with a second-half rebound, they’d end up basically unchanged.

He suddenly had plenty of company, too.

Last year’s selloff, sparked by the rate hikes, spooked strategists. By early that December, they were predicting that equity prices would drop again in the year ahead, according to the average estimate of those surveyed by Bloomberg. That kind of bearish consensus hadn’t been seen in at least 23 years.

Even Marko Kolanovic, the JPMorgan Chase strategist who had insisted through much of 2022 that stocks were on the cusp of a rebound, had capitulated. (That dour sentiment has extended into next year, with the average forecast calling for almost no gains in the S&P 500.)

It was Wilson, though, who became the public face of the bears, convinced that a 2008-type crash in corporate earnings was on the horizon. While traders were betting that cooling inflation would be good for stocks, Wilson warned of the opposite — saying it would erode companies’ profit margins just as the economy slowed.

In January, he said even the downbeat Wall Street consensus was too sanguine and predicted the S&P could drop more than 20% before finally snapping back.

A month later, he warned clients the market’s risk-reward dynamic “is as poor as it’s been at any time during this bear market.”

And in May, with the S&P up nearly 10% on the year, he urged investors not to be duped: “This is what bear markets do: they’re designed to fool you, confuse you, make you do things you don’t want to do.”

A stalled housing construction project in Zunyi, Guizhou province, China, on June 15, 2023. Photographer: Qilai Shen/Bloomberg

A stalled housing construction project in Zunyi, Guizhou province, China, on June 15, 2023. Photographer: Qilai Shen/Bloomberg