By

By  October 11, 2023 at 01:43 PM

October 11, 2023 at 01:43 PM

What You Need to Know

- Most advisors consider the stock of a client's employer a risky asset.

- Many advisors appear comfortable with larger allocations to employer stock than to other risky assets.

- While research suggests holding little or no employer stock, there are behavioral aspects to consider.

Owning employer stock is typically considered relatively risky, due not only to the risks associated with owning a single security, but also given the positive correlation to other sources of investor wealth (i.e., human capital).

While research on optimal household allocations to employer stock typically suggest portfolio weights should be incredibly low or zero, financial advisor perceptions regarding the potential risks are likely to vary.

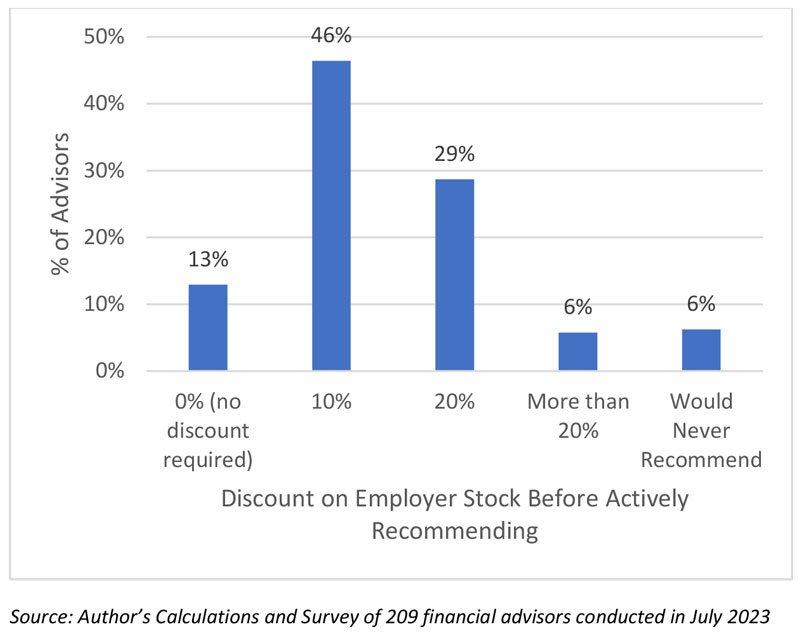

In a recent survey of financial advisors, I find notable differences in the perception of risk of owning employer stock, although there is relative consensus that allocations to employer stock should be less than 10% of an investor’s total financial assets and that there should at least be a 15% discount before purchasing.

Since there isn’t one “right answer” in terms of appropriate allocations, it’s important for financial advisors to take a thoughtful approach when providing guidance to clients regarding owning employer stock, especially when considering the various behavioral and economic implications of doing so.

Allocating to Employer Stock

I recently worked with my colleagues in Prudential’s Marketing Insights & Analytics group to field a survey among financial advisors. The survey was conducted from July 10 to July 14, and 209 financial advisors responded. The survey covered a variety of topics, with a specific subset focused on allocations to employer securities.

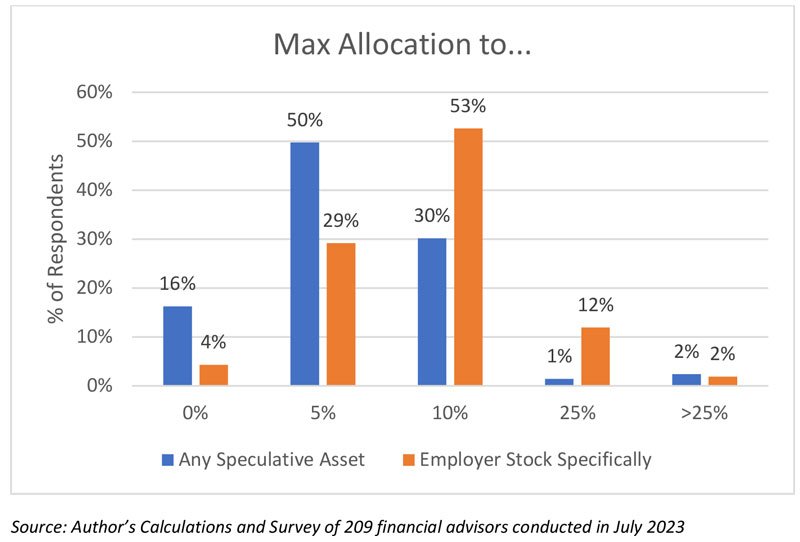

Two questions focused on the maximum percentage of a client’s total investable assets the advisor would feel comfortable allocating to speculative assets. One focused more generally on maximum allocations to “speculative assets” (which explicitly noted cryptocurrencies as an example), while the other asked only about maximum allocations to employer stock. The graphic below includes the distribution of responses to the two questions.

There are clearly differences of opinion among advisors when it comes to maximum allocations to speculative assets more generally or employer stock more specifically. To generalize the findings, though, it looks like while advisors try to limit allocations to more speculative assets, like cryptocurrencies, to no more than 5% of assets, they are more comfortable with allocations to employer stock, where they try to limit maximum allocations to 10% of financial assets.