August 12, 2022 at 02:41 PM

August 12, 2022 at 02:41 PM

Just like old times. That’s what it must seem like with the S&P 500 Index up about 15% since mid-June and poised for its fourth consecutive weekly gain, its longest winning streak of the year.

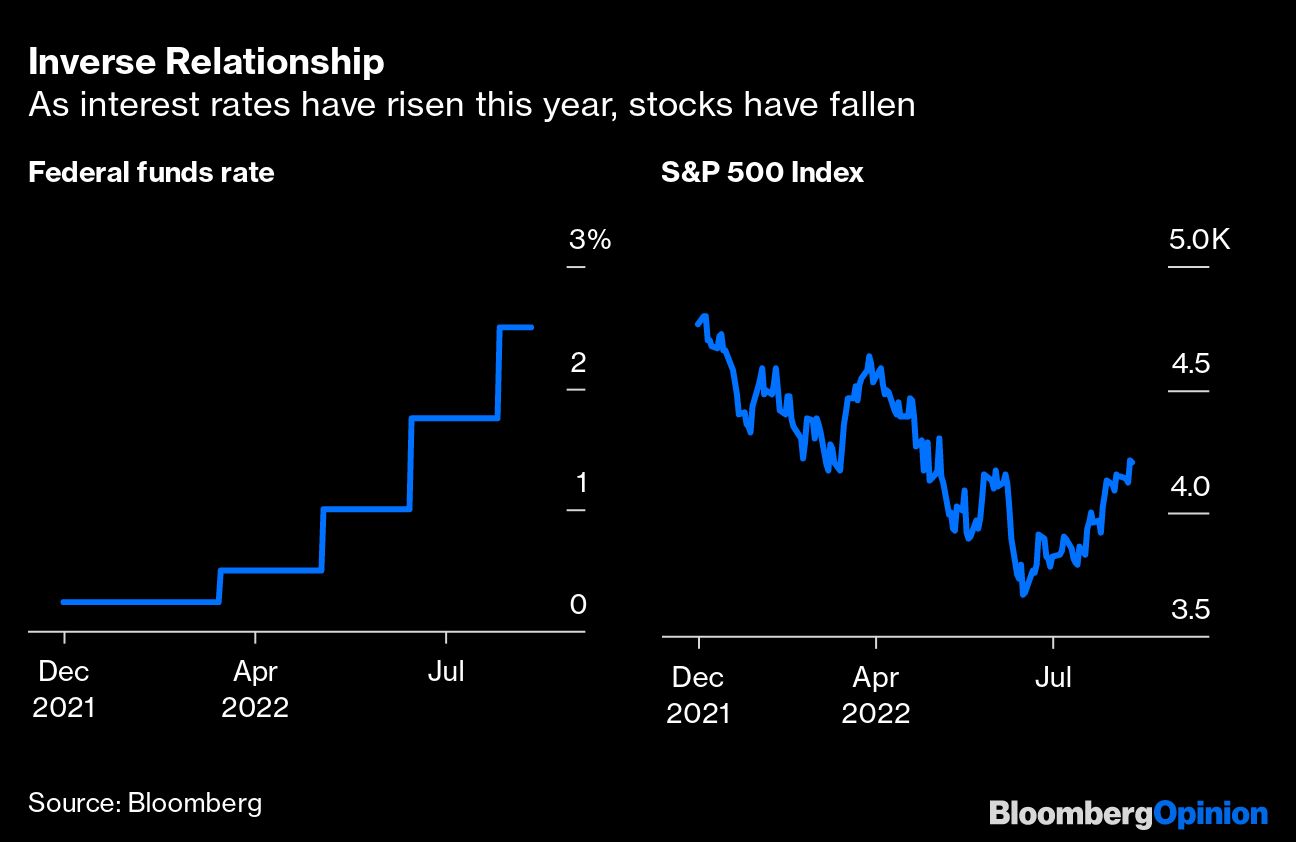

Those who question the durability of this rally, given the slowdown in the economy and a Federal Reserve that has doubled down on its plan to keep raising interest rates, can take comfort in one key metric: the smart money.

That can be seen in the Smart Money Flow Index, which measures action in the narrower Dow Jones Industrial Average during the first half-hour and the last hour of trading.

The thinking is that the first 30 minutes represent emotional buying, driven by greed and fear of the crowd based on good and bad news as well as a lot of buying on market orders and short covering. The “smart money” institutional investors, though, wait until the end of trading to place big bets when there is less “noise.”

That gauge has risen to its highest level in two years, when animal spirits ruled Wall Street and the S&P 500 was surpassing its pre-pandemic highs, sparking one of the most powerful bull markets in history.

Few are anticipating a repeat performance, but the latest trading patterns should provide some confidence that the nasty selloff in the first half of the year, which pushed stocks into a bear market, may be over.

The reasons for the rebound are clear. Gasoline prices have fallen every day since peaking at $5.016 a gallon on June 13, dropping all the way to $3.99 amid a broad decline in commodities prices and alleviating substantial pressure on consumers. Companies have reported solid second-quarter earnings.

The labor market remains unusually tight, with 528,000 jobs added in July, more than double the median estimate in a Bloomberg survey. There’s even optimism that perhaps inflation has peaked and will start to slow after the government said this week that its consumer price index was unchanged in July from the month earlier.

All this is bolstering the case for a so-called soft landing of the economy, in which the Fed is able to continue to raise interest rates, albeit more slowly, to get inflation back under control without causing a deep, long and nasty recession.

“Such a moderation in the Fed’s messaging and actions would be positive” for stocks, David Kelly, the Chief Global Strategist at JPMorgan Asset Management Inc., wrote in a research note earlier this week.

Granted, this is just one metric, but the rise in the Smart Money Index has been corroborated by another other key measure. State Street Global Markets, which has about $38 trillion of assets under custody or administration, said its North America Investor Confidence Index rose in July by the most since February, putting it back in bullish territory.

The reason this measure is worth heeding is because it’s derived from actual trades rather than survey responses.

All this is not to say that there aren’t plenty of headwinds ahead for stocks. For one, the Fed is nowhere near done raising rates.